India’s Leapfrogging Energy Transition: Sustaining Economic Expansion, Enhancing Grid Reliability, Flexibility, and Achieving Net Zero Policy Goals

Explore how leapfrogging India's energy transition is pivotal for its economic growth and NetZero ambitions. This article delves into India's journey towards a flexible energy grid, addressing challenges like grid reliability, renewable integration, and the role of next-gen technologies in achieving Prime Minister Modi's vision of a developed nation by 2047. Join us in understanding India's potential to transform its energy sector and sustain economic expansion.

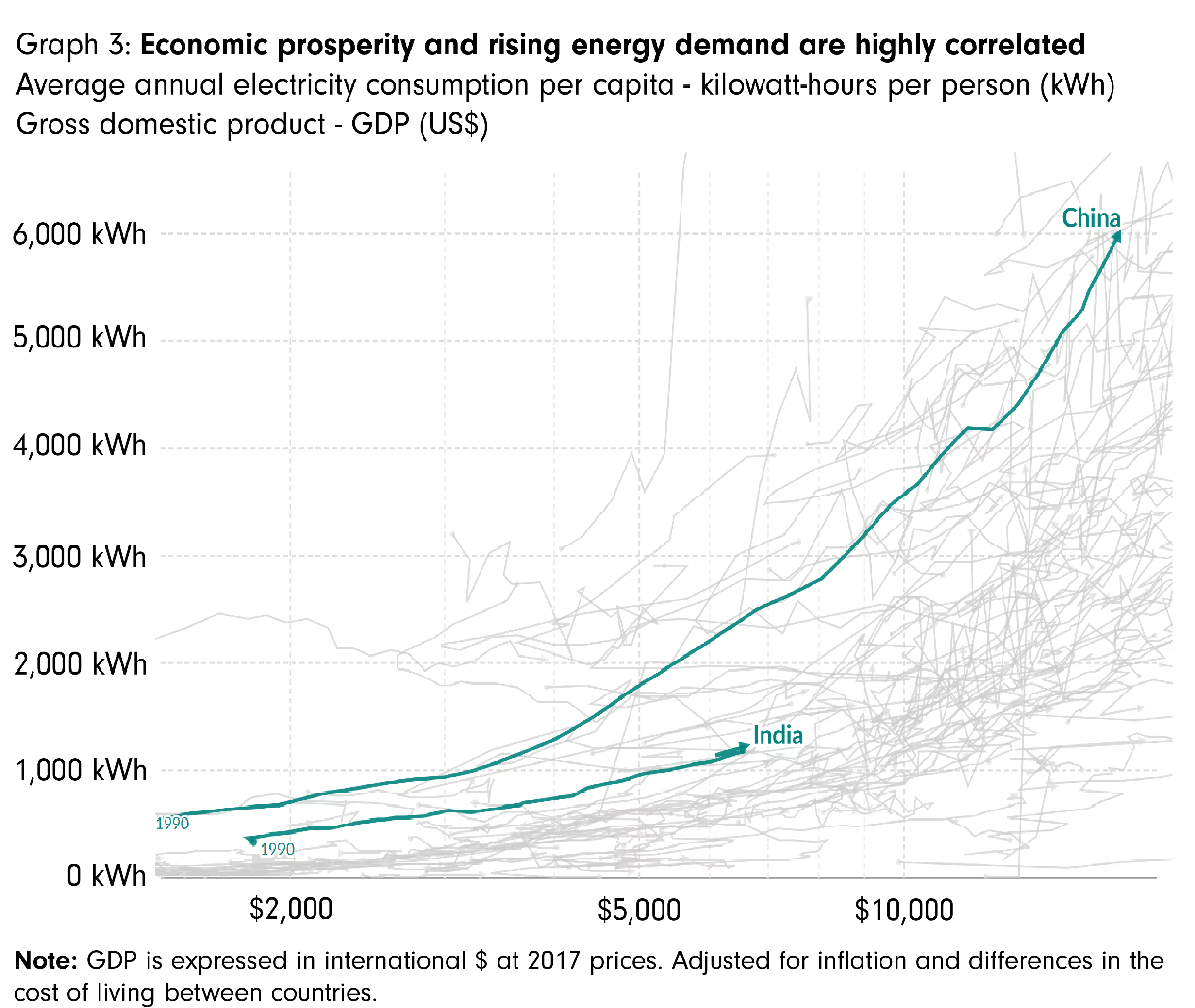

To achieve Prime Minister Modi's vision of India becoming a developed nation by 2047, its central bank set a high bar: an annual GDP growth rate of 7.6% for the next 25 years, a sustained and high rate of growth only last seen with China in the late 20th century. Achieving this goal hinges on substantial capital investment, rapid productivity growth, and, fundamentally, transformative reforms through leapfrogging India’s energy transition.

Despite ambitions of nationwide economic prosperity, parts of India are still stuck in the dark ages. A village in Pandaria district, Chhattisgarh, is one of many examples where, due to the lack of electricity, the livelihoods of people have suffered, adversely impacting economic growth and labor productivity. While the government has earmarked billions to provide continuous energy supply to rural India, electricity unreliability remains a pressing theme.

While not every nation can effectively pursue technology leapfrogging, we firmly believe that India has the greatest potential among developing nations to adopt innovative technologies within the energy sector and adapt them to its unique circumstances. Let’s delve into India's potential to catalyze a transformation in its energy sector.

The Next Step in Electrification: Improving Grid Reliability

To sustain India's nationwide electrification momentum and rectify the unreliability of its grid system, it is imperative to make critical investments in next generation grid technologies.

Addressing Soaring Energy Demand with Grid Flexibility

With the growth of India’s economy and the associated rise in disposable income, more households are set to increase their adoption of various energy-consuming devices, further driving electricity demand. According to the IEA World Energy Outlook 2023, India’s demand for electricity to run household air conditioners is estimated to expand nine-fold by 2050, outpacing the growth in every other major household appliance (Graph 4a). In the IEA’s stated policies scenario (STEPS), cooling equipment is forecast to account for nearly half of the increase in India’s marginal electricity peak load demand increase from 2022 to 2030 (Graph 4b).

Electric vehicles (EVs) are also energy-consuming devices anticipated to be a meaningful driver of electricity demand in India. According to Bain & Company’s India Electric Vehicle Report 2023, India’s EV market is at an inflection point, with penetration expected to grow eightfold by 2030, jumping from 5% to 40%. EVs are a significant consumer of electricity – for example, the average kWh usage per year a Tesla Model 3 is 3,566 kWh. This is more than double that of a central air conditioning unit for a small home, which uses an average of 1,485 kWh per year.

A challenge posed by energy-consuming devices such as air conditioners and EVs is their potential to impact the electricity load curve, causing spikes in demand at certain times of the day. If not effectively managed through a flexible grid, these spikes could overwhelm the grid's capacity, leading to substantial grid constraints. This issue was highlighted in a 2022 California case study, which showed that the increasing number of electric vehicles (EVs) in the state of California is expected to strain the electricity distribution infrastructure due to the rising demand for electricity. Consequently, with more energy-consuming devices being connected to India's grid, having a flexible grid that can automatically adjust energy loads over certain time periods is a necessity.

The growing demand for electricity in India, fueled by economic growth and the increasing adoption of energy-consuming devices like air conditioners and EVs, highlights the urgent need for substantial capital investments in India’s grid infrastructure. These investments are crucial for expanding the electricity supply and increasing the grid's flexibility to handle peak electricity load demand within the network.

Integrating Cost-Effective Renewable Energy with Modernized Grid Infrastructure

Despite the clear cost-effectiveness of renewable energy, a crucial question arises: Why has India not already shifted away from coal? The answer lies in years of insufficient investment, which have resulted in an underdeveloped and outdated grid infrastructure. This means India’s grid is currently unable to handle the intermittent nature of renewable energy, necessitating grid modernization to effectively harness this inexpensive and clean energy source.

India possesses a substantial opportunity to shift towards renewable energy, a move that is not only cost-effective but also aligns with the country's ambition to achieve its net-zero goal by 2070. To capitalize on this opportunity, significant investments in grid modernization are paramount. Such investments would enable the adoption of cutting-edge technologies essential for effectively integrating intermittent renewable energy sources.

From Challenge to Opportunity: Leapfrogging India’s Energy Transition Through Limited Grid Infrastructure

Historically, India has garnered a reputation for underinvesting in its infrastructure. Decades of underinvestment have resulted in significant deficiencies in crucial sectors, such as electricity generation. The absence of adequate infrastructure has been identified by business leaders as a key limiting factor hindering both economic growth and corporate performance.

However, in recent years, India has taken great strides towards revolutionizing its infrastructure. In 2023, the Indian government allocated nearly 20% of its budget on capital investments, the most in at least a decade. Infrastructure spending has witnessed a substantial increase, surging from under 2 trillion rupees (US$24 billion) in 2014 to nearly 8 trillion rupees (US$96 billion) in 2023 (Graph 6). The surge in government infrastructure spending has had a notable impact on Indian stocks. In 2023, the S&P BSE Industrials Index, encompassing companies involved in a wide range of activities from bridge construction to wind turbine manufacturing, soared by over 50%, reaching an all-time high. This remarkable growth has notably outpaced the broader S&P BSE Sensex, underscoring the market's positive response to India's infrastructure advancements.

Moving forward, India has allocated significant resources to accelerate the improvement of its energy and grid infrastructure:

The Smart Meter National Programme (SMNP), established by the Government of India, aims to improve billing and collection efficiencies and pave the way for a more robust smart grid system. The SMNP targets the installation of 250 million smart meters by 2026. Assuming one smart meter per household in India (which had 302 million households as of 2021), the projected smart meter penetration among households would reach 83% by 2026, representing a substantial increase from the 2% recorded in 2021.

Despite India's goal of equipping more households with smart meters, this effort falls short in light of the country's current and future energy requirements. The projected growth in energy demand, coupled with the increasing number of energy-consuming devices needing grid connections – which will necessitate grid flexibility – and the demand for a modern grid capable of efficiently integrating clean energy, presents a compelling case for transitioning not just to smart grid technologies, but to next-generation grid technologies. India's current deficiencies in energy and grid infrastructure offer a unique opportunity to sidestep the constraints of grids in developed nations by developing an entirely new grid tailored for renewable energy integration, one that is both reliable and flexible. This approach could enable India to 'leapfrog' to a more sophisticated, renewable-centric infrastructure.

India's Grid Revolution: Navigating Financial and Capital Challenges

While there is significant potential for India to revolutionize its grid through technology leapfrogging, two structural challenges persist: (1) the financial health of Indian energy distribution companies, and (2) the cost of capital for renewable energy projects. The IEA has a similar take, stating: “…challenges related to high perceived risk and cost of capital, as well as to poor financial health of utilities, are hindering investments in grids across many countries”.

DISCOMs Struggle with Financial Losses and Grid Improvement Incentives

In a report published June 2023 by the Climate Policy Initiative, the cost of debt and required rate of equity return for renewable energy projects in India is 11.4% and 17.2%, respectively (Graph 11a-11b). This compares to the United States, with a cost of debt and required rate of equity return of 5.3% and 10.3%, respectively. India’s cost of capital sets a relatively high bar for renewable energy projects to raise debt finance and offer sufficient returns on equity.

India's journey towards economic growth and becoming a developed nation by 2047 is intricately linked to its ability to transform its energy sector through technology leapfrogging. Despite achieving near-nationwide electrification and significant poverty reduction, India faces challenges such as unreliable electricity supply and substantial transmission and distribution losses, which hinder GDP growth. The demand for electricity in India is surging, driven by industrialization and the increasing number of energy-consuming devices connecting to the grid. Renewable energy, particularly solar and wind, offers a cost-effective alternative to coal and a pathway to achieve India’s net-zero goal, but their integration requires modern grid infrastructure.

India's potential for smart grid technology leapfrogging is significant, given the existing grid infrastructure gaps and substantial capital commitments. However, challenges such as the financial health of distribution companies and the high cost of capital for renewable energy projects pose structural hurdles. Overcoming these challenges will be crucial for India to leverage its considerable capital investments effectively and realize the full potential of next generation grid technologies. This energy sector transformation is essential not only for India's economic growth but also for its ambition to play a leading role in global energy dynamics and climate change mitigation.

India has momentum. As the world watches, India is not just poised to technology leapfrog; it is ready to soar.

About The Author

Colin Tang is the Senior Investment Officer at Corinex, where he leverages his extensive experience in finance to drive the company's investment strategy and portfolio performance. With a proven track record of identifying and capitalizing on investment opportunities, Colin plays a crucial role in supporting Corinex's financial objectives and growth.

Contact us to request access to the data and analytics mentioned in our article, or discover how Corinex solutions enable grid digitalization and address grid constraints.

Stay ahead in the energy game! Subscribe to our CoriNEXT newsletter and get the latest trends on grid visibility and flexibility, policy updates, expert tips, and workshop opportunities - straight to your inbox.

Subscribe to CoriNEXT for the latest on grid visibility, flexibility, expert insights, workshops, and the future of grid modernization.