The U.S. power system is entering one of the most capital-intensive periods in its history. Investor-owned utilities are expected to deploy more than US$1.1 trillion across grid and generation infrastructure between 2025 and 2029, nearly matching the US$1.3 trillion invested over the previous decade.

Yet the pace of expansion is no longer dictated by funding. It is increasingly constrained by the availability of critical equipment.

Large power transformers (LPTs), essential to stepping voltage across transmission and distribution networks, have emerged as a binding bottleneck. More than 90 percent of power consumed passes through a LPT at some point, making them foundational to both system reliability and incremental capacity buildout. As a result, transformer availability, not capital allocation, is becoming the limiting factor in how quickly the grid can expand.

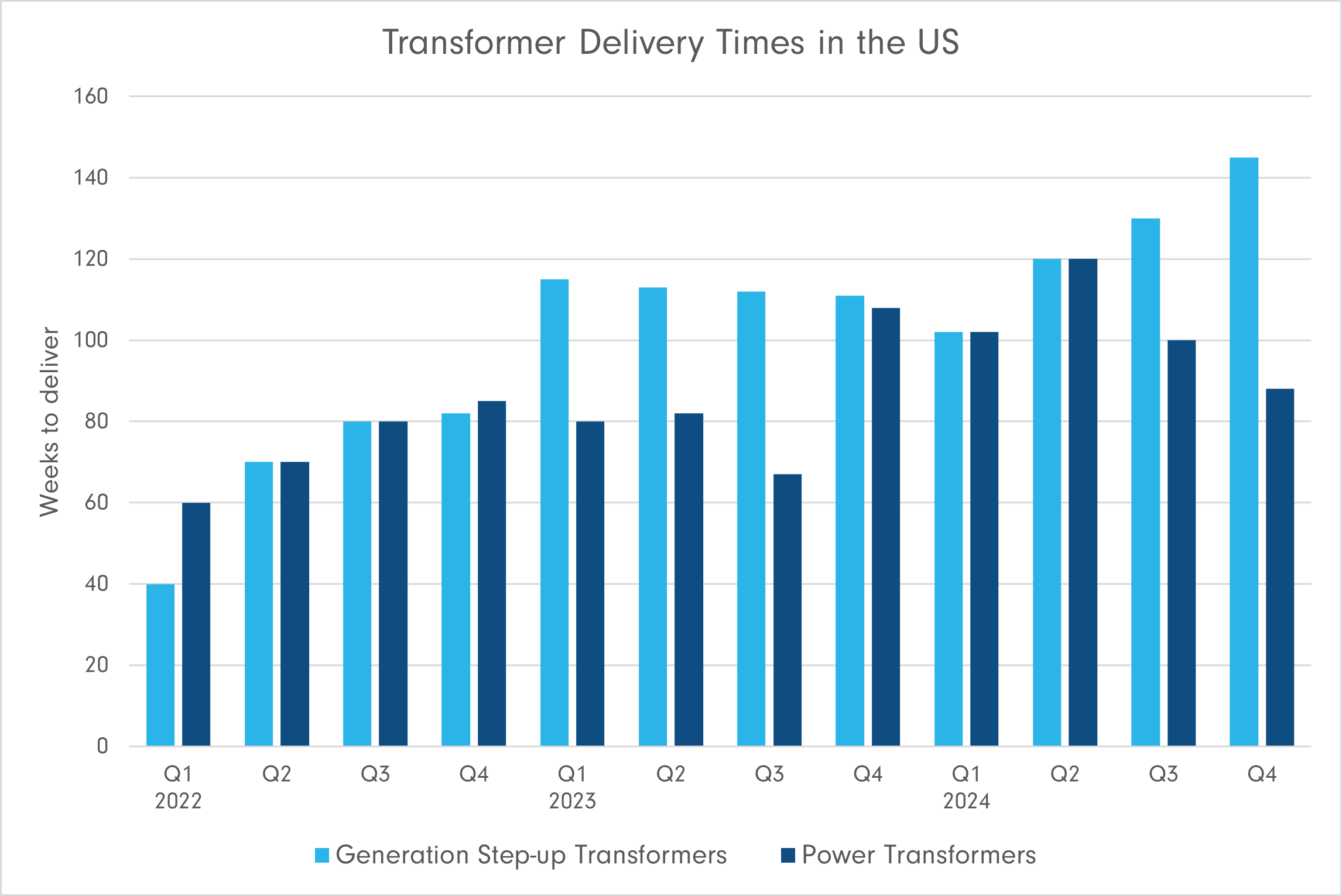

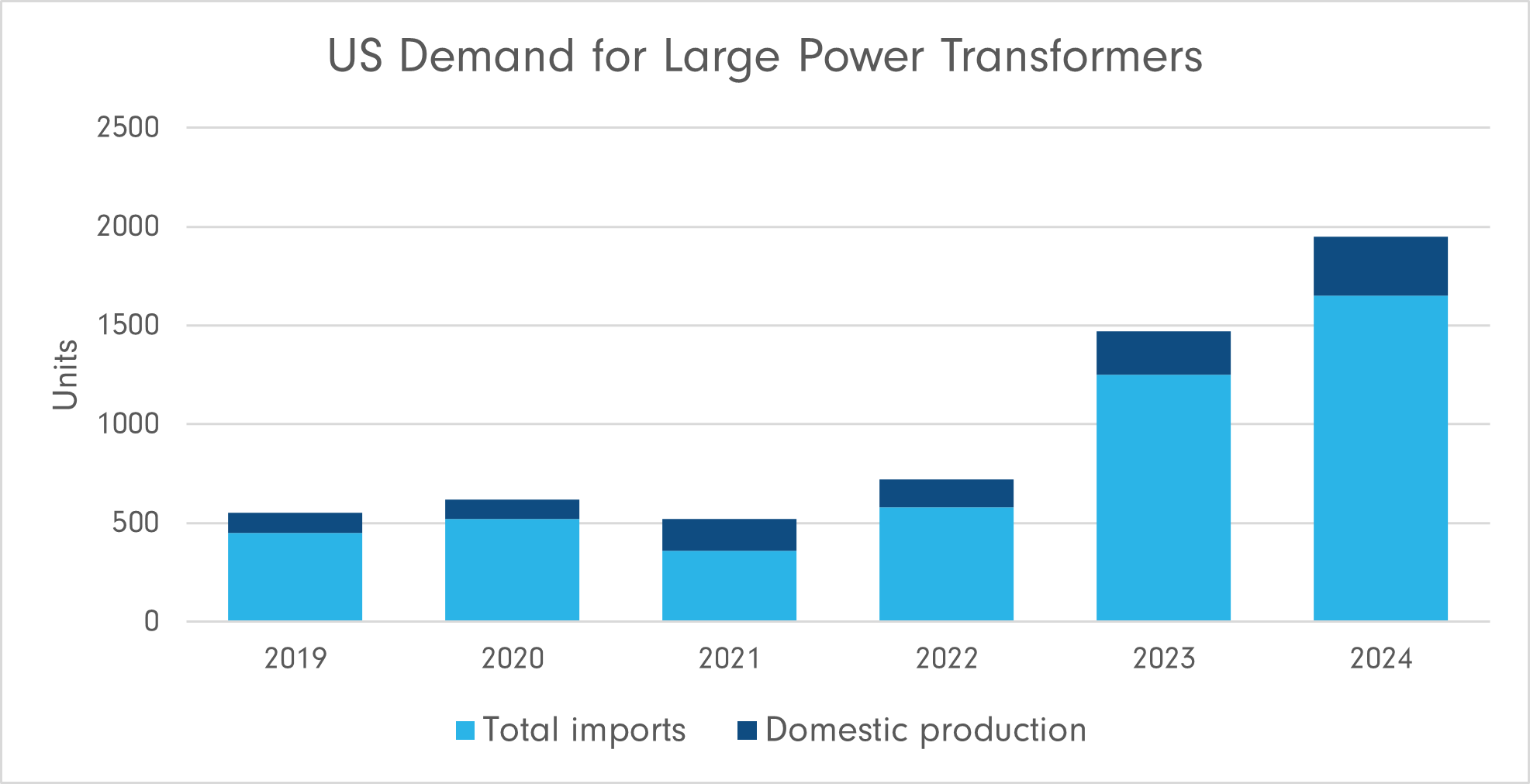

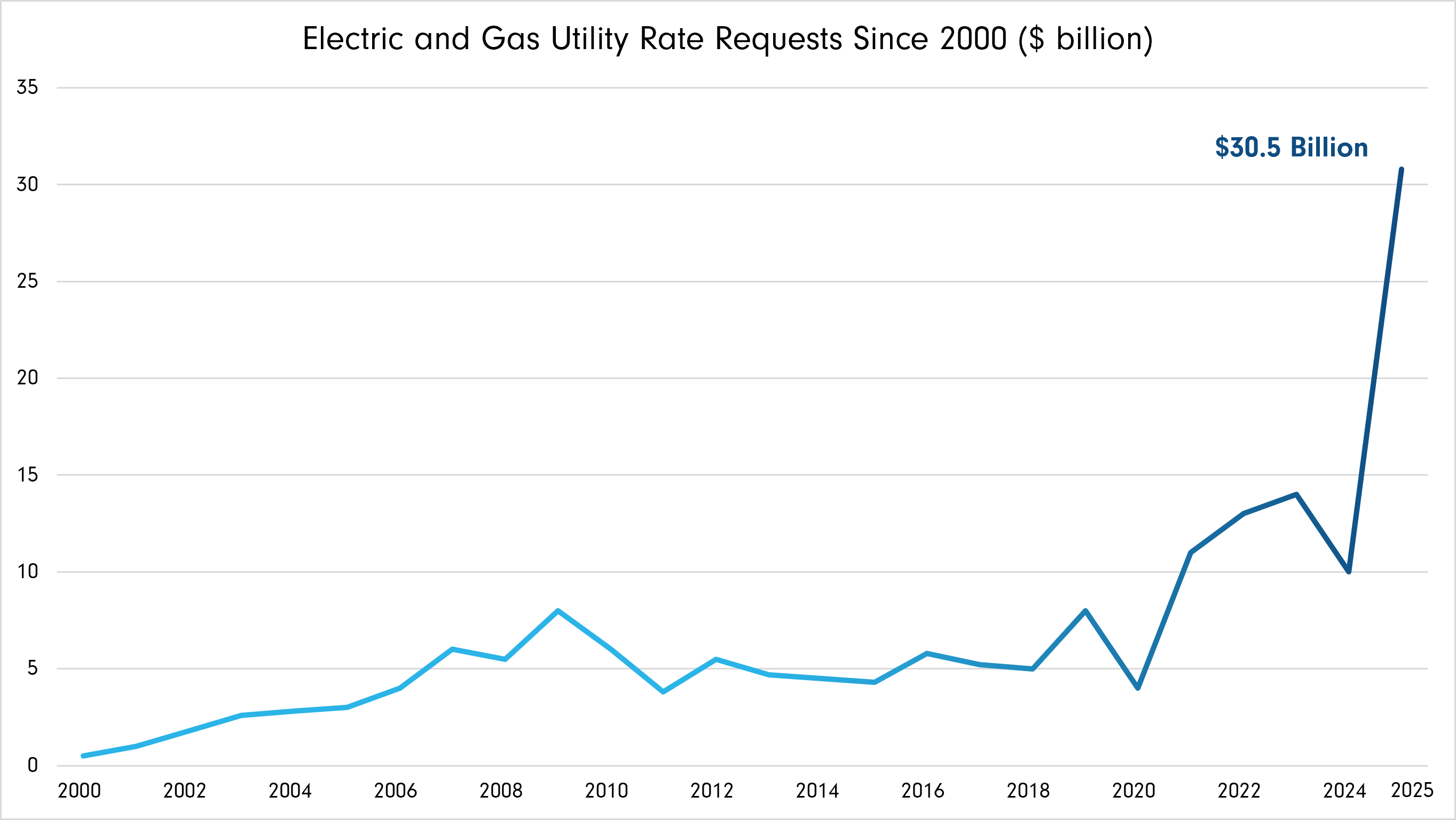

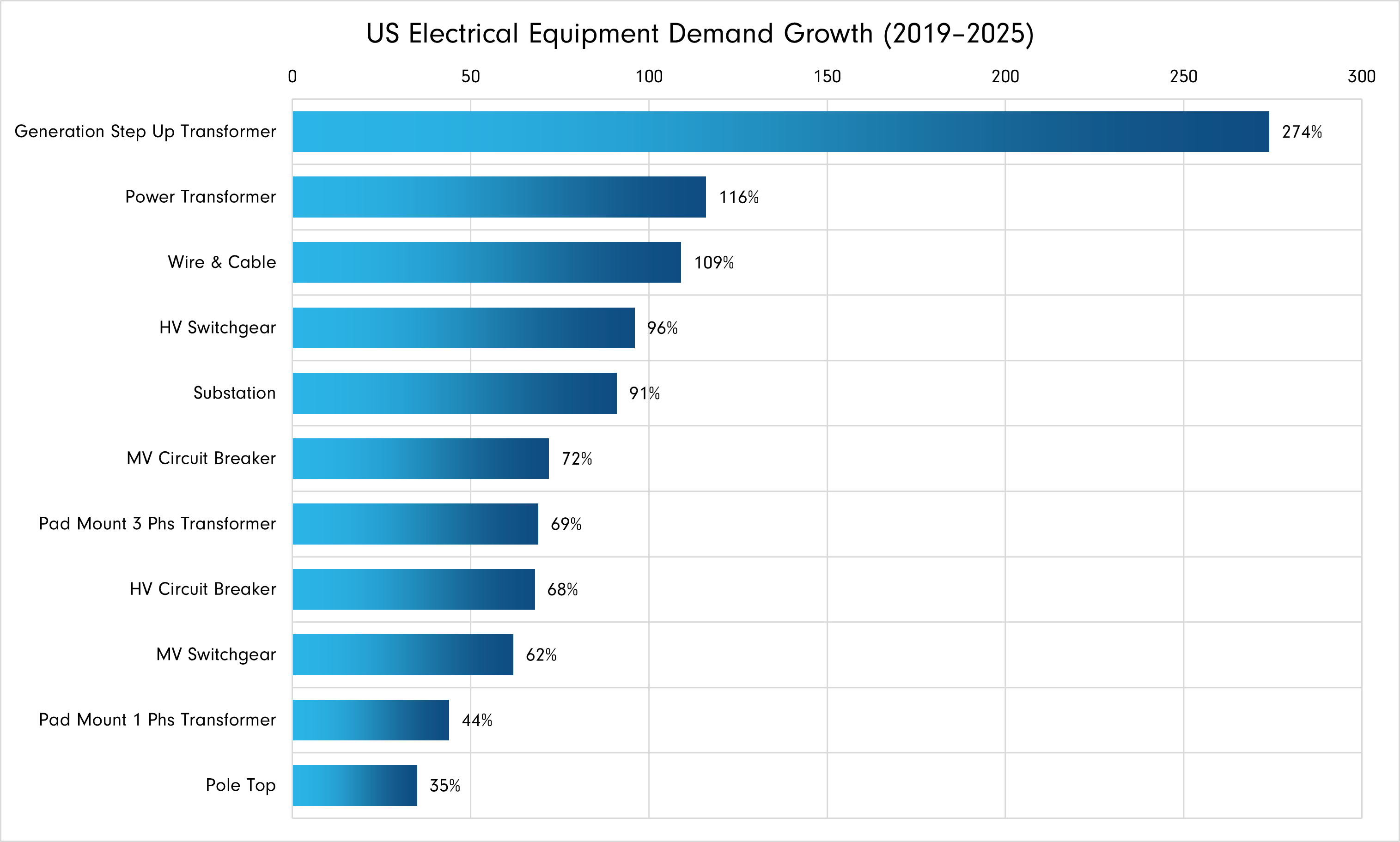

Demand for LPTs is rising simultaneously across multiple fronts (Graph 1). Nearly 2,300 gigawatts of generation and storage capacity remained in interconnection queues at the end of 2024, while the existing transformer fleet continues to age, with average asset lives approaching 40 years, near the end of their useful life. At the same time, load growth tied to data centers and artificial intelligence is accelerating, introducing a more concentrated and less predictable source of demand relative to traditional load growth.

Graph 1: U.S. grid demand drivers increasing pressure on large power transformer supply

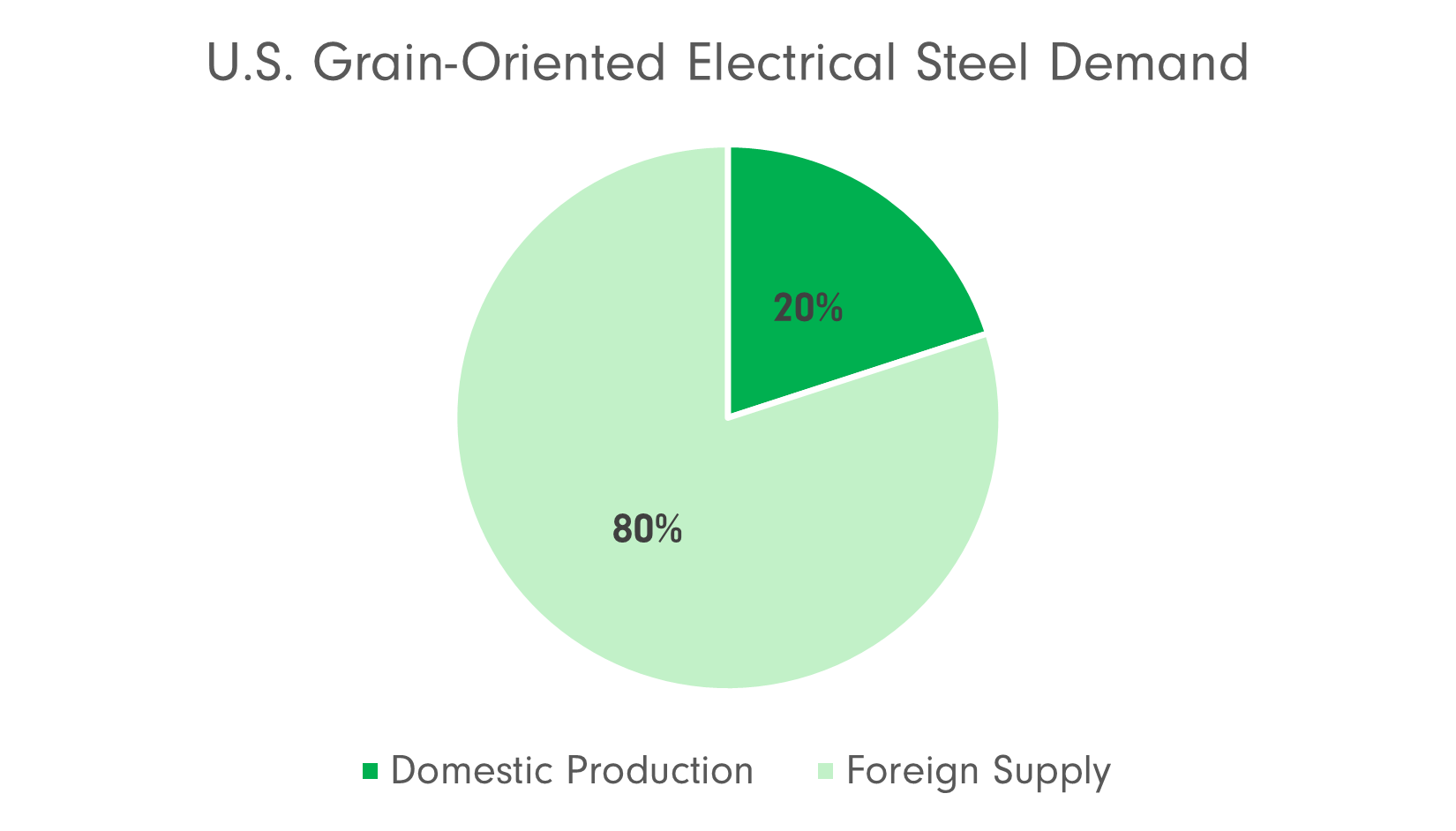

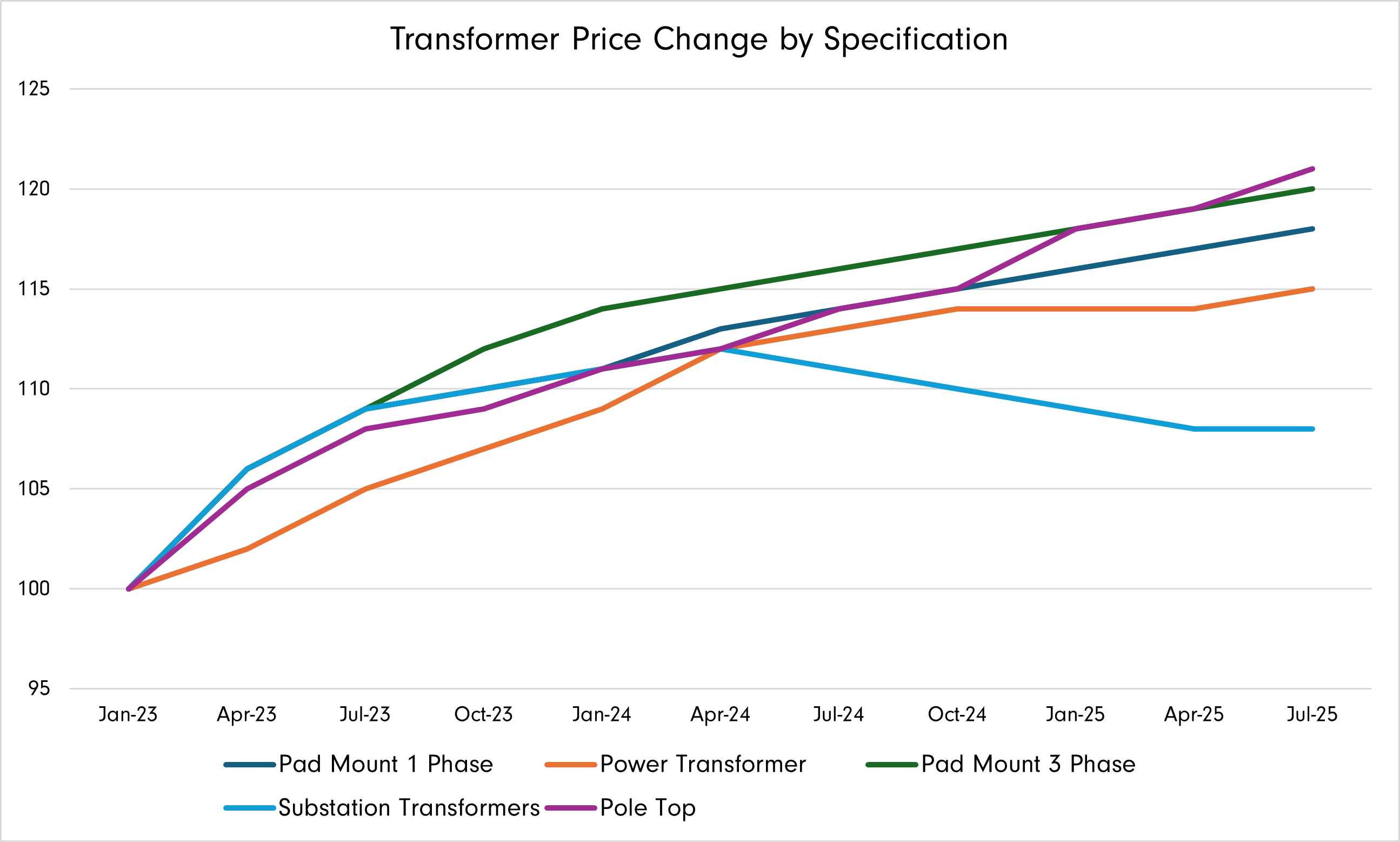

The supply of LPTs has not kept pace. Limited domestic manufacturing capacity, dependence on specialized inputs, and elevated costs have extended procurement timelines from months to multiple years. For utilities, this reduces flexibility to replace aging assets and delays the integration of new generation, creating a widening gap between capital deployed and infrastructure delivered.

The implication is structural: even sustained increases in capital expenditure are unlikely to translate into proportional gains in grid capacity unless transformer supply expands materially.